The international media is jabbering about the Greek economic crisis. Lots of words, very little clarity. Professor Anil K Kashyap offers help in this blog today. If this is a (fair & balanced) dismal story, so be it.

[x Booth School of Business — University of Chicago]

A Primer On The Greek Crisis: The Things You Need To Know

By Anil K Kashyap

Tag Cloud of the following piece of writing

1) How did Greece get into such trouble?

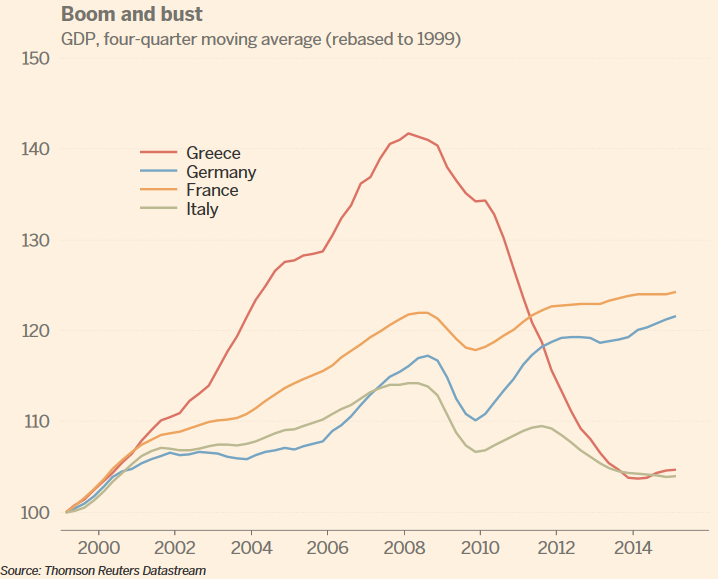

Greece from the mid-1990s until last year was constantly spending more than it was collecting in tax revenues. For most of this time, the country’s initially reported numbers showed small differences that were subsequently found to have been much larger. The revisions tended to be most substantial right after elections when a new government would find that its predecessor was much more profligate than had been reported. Because of these deficits, the country borrowed to cover the shortfalls and its debt burden was steadily rising.

In the fall of 2009, a then newly elected government reported that the deficit for that year was going to be 13.6 percent of economic output and that the deficits in 2007 and 2006 were also larger than had been reported. From that point onward, the world began to wonder if Greece really could pay the debt that it had issued or needed to default. Its borrowing costs rose sharply and the country began looking for ways to reduce its required debt payments and end its borrowing addiction.

2) Wasn’t Greece already bailed out in 2010?

By the spring of 2010 the excessive debt problem became unbearable and there was open speculation that Greece would default. The country had done this on four occasions previously since 1800. Much of the government debt was owed to banks outside of Greece, with the largest amounts in France and Germany. So if Greece had stopped paying, the French and German banks would have suffered substantial losses.

Greece was lent new money in 2010, but as Karl Otto Pohl former head of the German central bank observed at the time much of that money was used to repay the obligations owned by the French and German banks. The new lending was advertised by the politicians across Europe as a rescue for Greece.But it was at least as much a deal to buy time for the banks and other owners of Greek debt to avoid a default. Greece did avoid default, but the support came with requirements designed to make sure that the country end its chronic deficit spending

.

3) Why did that rescue fail?

To justify the new lending, the lenders had to be assured that the deficits would end and that the country would grow enough to be able to service its debt. In May of 2010, the International Monetary Fund (IMF), led at the time by Dominique Strauss Kahn, who had ambitions of running for the presidency of France, conducted an analysis to see if such a scenario was realistic. The report at the time concluded that if Greece undertook drastic reforms it could close its deficits and begin growing so that over time the debt (including the new lending that was being provided) would be manageable.

This analysis was later shown to be deeply flawed by the IMF itself [PDF]. The Greeks did actually cut their deficits substantially, but many of the reforms that were supposed to support growth did not occur and the economy contracted substantially. So the debt, relative to the size of the economy, did not improve. Importantly, no debt was written off in 2010, even though many analysts, including some on the executive Board of the IMF, at the time believed that it was necessary and that the banks and other private sector owners of the debt should have taken some losses.

4) What is the troika (or the institutions) and what do they have to do with this?

The new lending in 2010 came from two sources, a fund that was raised from European governments and the IMF. The bailout fund was overseen by the finance ministers of these governments. The European Central Bank also provided support to Greece in two ways. First, it allowed banks in Greece (and everywhere else) to borrow from it by posting bonds guaranteed by Greece as the collateral. Second, it bought some Greek government bonds in the open market. So all three of these organizations were now exposed to losses in the event that Greece ever defaulted. As such, they had representatives that met regularly with the Greek government to make sure that the reforms were on track. Initially the three were called the troika. Subsequently, they have also been referred to as “the institutions”.

5) Wasn’t Greece also bailed out in 2012?

By late 2010 it was already clear that the debt burden might prove to be unsustainable. So discussions began over reducing the debt. The Greek government was supposed to sell some assets to retire some of the debt. That never happened and as the recession continued it was clear that the 2010 plan was not going to be adequate. So in March 2012 a second bailout program with revised terms was undertaken.

The IMF lent additional money, but the main conditions that accompanied the funding were largely the same. Once again, the cornerstones of the plan continued to be steps to make tax collection more efficient, to reduce spending promises, and to undertake reforms to encourage hiring and business expansion that would support growth. It was not clear why this plan would be more successful than the first one.

The European Central Bank meanwhile became more deeply committed to stabilizing financial markets. ECB President Mario Draghi famously said in July 2012 that “within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough.” Draghi’s statement immediately led to a drop in borrowing costs for governments across Europe and the pressure on Greece temporarily subsided.

By continuing to allow banks everywhere to use Greek debt as collateral, the ECB also created conditions that supported the trading of Greek debt. By this time the French and German banks had shed their exposure to Greece so that they would no longer be directly harmed if there was a default. So the stealth rescue of the non-Greek banks was completed with little public attention and the narrative that all the problems were self-inflicted by the Greeks became more pronounced.

6) Why is Greece in trouble again now?

In the time since Draghi’s statement three important things happened in Greece. First, Greece made further substantial progress on closing its deficits. By late 2014, Greece was finally spending less than it was collecting, although the interest payments on debt meant there was still an overall deficit. So for the first time since Greece adopted the euro it had budget position that was solid.

Second, the economy contracted for two more years as the reforms failed to deliver higher growth. Certainly the higher tax collections and reduced government spending contributed to the weak performance, but the degree to which the planned reforms, if fully implemented, could have offset that remains controversial. It is important to also recognize the massive collapse was preceded by a very large debt-fueled boom.

Austerity notwithstanding, the economy seemed to have reached bottom and was finally beginning to recover in late 2014. A very interesting counterfactual scenario is to contemplate what would have happened if the political situation had allowed this progress to continue.

The third major development, however, was that the public lost confidence in the incumbent government and its lenders. Unemployment in Greece has remained above 25% for years and was much higher for young people. So the citizens were fed up. Hence, in 2015 the public voted for a new government that insisted on deviating from the past playbook.

The major party in the new coalition, Syriza, is often referred to a coalition of the radical left. In January 2015, newly elected Prime Minister Alexis Tsipras sought to reopen negotiations with Greece’s creditors.

7) What is the Greek government asking for?

The Tsipras government wanted three types of changes. First, it wanted to restore some of the spending cuts that had been enacted. Second, it wanted to reverse some of the revenue hikes that the past governments had instituted. These first two requests would have widened the deficit and also reorganized priorities within the budget. (In fact, once it became clear that Syriza was going to win the election, tax revenues began shrinking as the public stopped paying some unpopular taxes).

Finally, it wanted outright forgiveness of some of the debt that had accumulated.

Since taking office, Tsipras has been negotiating with the creditors over for a new set of agreements. The creditors have made some modest concessions but are largely insisting on a continuation of similar plans.

When he failed to secure these changes, Tsipras announced that he would have the Greek people vote on a referendum on July 6th over whether Greece would vote yes to accept the creditors latest offer or vote no to reject it.

8) Why do the institutions disagree with the government?

There are two sources of objections that the creditors have with Tsipras’ requests.

First, and probably most importantly, countries such as Italy, Portugal, Spain, and Ireland, had all had to undertake similar types of adjustment as in Greece. None of them saw their economies collapse to the extent of Greece, but unemployment especially among the young is also high in all these countries. Hence, if there are substantial concessions to Greece, then these countries will insist upon getting similar treatment. The existing governments in these countries all realize that if electing a radical government in Greece is seen as being rewarded, then voters elsewhere will do the same.

The money needed to save Greece could easily be found. Greece is a small economy, so even though their debt is large when judged relative to Greece’s economy, it is small relative to the overall capacity in Europe. In contrast, the money needed to forgive debt in the other countries, especially Italy and Spain, is not affordable for Germany (and all the other Northern European countries that would have to foot the bill).

Second, even if there was some way that Greece could be helped without setting a precedent, the officials do not trust the Greeks to carry through with any plans. The fact that Prime Minister Tsipras is asking for a public referendum to accept a continuation of prior policies was the straw that broke the camel’s back. Tsipras is arguing that the public should reject the plans, but he says that if the public prefers to accept them, then he will go along with that. The institutions doubt that he could reverse his position and suddenly begin taking steps which he has campaigned against for years. They also are infuriated that he believes his mandate to get better terms supersedes the ones that other elected governments had from their citizens that wanted no more bailouts.

Another consideration is that IMF, the ECB and the other European leaders believe that unlike before if Greece defaults the spillovers can be managed.

9) Why is the IMF loan that is coming due so important?

The IMF made loans in 2010 to Greece that no private lender would have been willing to make. It did so with the presumption that it would be first in line to be repaid subsequently.

For failing businesses in many countries, there is analogous arrangement where in a bankruptcy situation a judge can decide that a business is worth more if it can continue to operate with some new funding, than if it was closed and sold off immediately. In that case, the new funding gets highest priority for repayment (otherwise no one will lend) and a judge will make sure that is the case. For countries, enforcing this priority is a problem since there is no court or other authority that can compel a country to pay.

Greece has now announced that it will not pay the IMF the €1.55 billion that it is owed on Tuesday (June 30); once it has defaulted, Greece becomes an international pariah. To preserve its own ability to operate in future crises, the IMF must insist on being repaid. If it ever accepts the idea that a country can default if things go south, then it will never get repaid in the future. So the IMF will continue to seek repayment, no matter how flawed the analysis that led to the lending in the first place.

Interestingly, Greece did make a small payment to the European bailout fund, so it will not be in default to that lender even if it does fall behind with the IMF.

10) What did the ECB decide this weekend and why is Greece closing its banks?

The ECB decided it could no longer keep accepting additional collateral from the Greek banks that was guaranteed by the Greek government. This means no more extraordinary lending will be extended. The ECB was worried that Greece might not honor the obligations and hence it could be left with collateral that would be insufficient to cover the loans it extended already. This is in keeping with Draghi’s promise of staying within the ECB mandate; lending when losses are expected would be clearly illegal.

However, the ECB has not completely cut off its support to Greece. The ECB could have recalled all of its loans, or demanded even more collateral for the existing loans. But for the Greek banks this removed the only viable option for obtaining more cash. They do not have assets that they can sell to come up with more cash. So without the ECB’s full support, they are in serious trouble.

Greece has closed the banks so that depositors cannot take out all of their money. There are now limits on how much depositors can get from ATMs and limits on wire transfers. So depositors are nervous and scared about what is going to happen.

11) What can Greece do to save its economy now?

Greece must either find a new lender, which seems very unlikely, or survive with very little credit for a while; Russia will not step in to offer support, since doing so would likely wind up with some of the resources transferred to other creditors and Russia has its own big fiscal problems.

If there is a no vote, Greece will likely stop payments on all debt. Being cut off from credit markets, it will now be forced to match its spending to the revenue it is receiving. To ease the burden, the government will likely distribute IOUs of some form to government employees, vendors and pensioners. It may even have to use IOUs to fund the referendum.

These IOUs will likely circulate as a form of money alongside the euro. People will strongly prefer euros to the IOUs, so the IOUs will trade at a discount.

Some people and businesses may resort to bartering.

12) Why not just bring back the drachma?

The public will have little confidence in the IOUs that the government issues. Probably even less confidence if Greece opts to officially introduce a new currency. Reintroducing the drachma would be totally illegal under European law and form the basis for a law suit to force Greece out of the European Union (EU). As part of the EU, Greek citizens can travel freely and work anywhere within Europe. Greek goods are also allowed to be sold without being subject to tariffs. Expulsion from the EU would be devastating.

Issuing IOUs which are not officially touted as a currency is a better option for Greece for now.

13) Will the Greek crisis spread?

It depends largely on what citizens make of the impending chaos in Greece. If people believe that their governments also might default on debt, they could also try to get money out of the banks. Likewise, investors could refuse to buy newly issued debt.

The ECB is likely to be able to head off both these problems. It is already buying debt and can do more of that. It also can lend against the collateral guaranteed by these governments. The ECB can probably contain the immediate fallout.

The political contagion is much harder to assess. Perhaps if Greece emerges in better shape in the medium term, then other countries will follow. Tsipras was betting that this concern would be so powerful that Europe would never take this risk.

14) What is likely to happen next in Greece?

The outcome of the referendum now becomes critical. If the public votes “yes”, then perhaps the existing government (likely reorganized) will be able to reopen the banks and conclude a deal.

But, if the public sides with Tsipras government, then there will be a very sharp recession over the next few months. Tax collection is likely to collapse. The Tsipras government is unlikely to survive the economic collapse.

If the post-Tsipras government opts to proceed with the default, then the next big unknown is how long before the economy stabilizes. At some point Greece will be a very attractive tourist destination, and its goods that are no longer priced in euros will be more competitive, so at some point the economy will begin to turn around. Whether this takes months or quarters will depend on many decisions that are difficult to forecast now.

15) What happens to the IMF if its loan is not repaid?

It will continue to pursue its claim against Greece. Greece will not be able to borrow internationally until it makes peace with the IMF. So the IMF will eventually be repaid. This could take years.

The IMF is likely to be criticized further for the recommendations it made, particularly in 2010. Perhaps it will be reformed to limit its discretion in lending.

Traditionally the head of the IMF has been a European. That is very likely to change since many countries believe that Greece was treated preferentially because it was a European country.

16) What happens to the ECB if Greece defaults?

The loans made to Greece are extended by the Greek central bank, which in turn borrows from the ECB. So the ECB will have a large claim against the Greek central bank that is likely to turn into a significant loss.

17) Can the ECB survive if Greece defaults?

The ECB can definitely continue even if Greece defaults. The ECB has provisions set aside to cover some losses. It also is making lots of profits on the bonds it owns (that it pays for with money that pays no interest). So the Greek losses per se are not a problem.

A default by a larger country such as Italy or Spain would be very different.

18) What should have been done to avert this crisis?

Greece should have defaulted in 2010. Its debt burden then was unsustainable and nothing since then has changed this. It is true that financial markets were much more jittery at that time, but the money that was raised to pay off the creditors in that bailout could have been diverted to support Greece and other weak countries. Once the bad rescue of 2010 was undertaken, it was inevitable that some form of debt relief was going to be necessary.

Imagine how different the political dynamics in Europe would have been if the German and French banks had been explicitly bailed out. Ω

[Anil K Kashyap is the Edward Eagle Brown Professor of Economics and Finance at the University of Chicago Booth School of Business. His research focuses on banking, business cycles, corporate finance, price setting, and monetary policy. His research has won him numerous awards, including a Sloan Research Fellowship, the Nikkei Prize for Excellent Books in Economic Sciences, and a Senior Houblon-Norman Fellowship from the Bank of England. Kashyap graduated from the University of California-Davis iwith a BA (economics and statistics with highest honors). He also received a PhD (economics) from the Massachusetts Institute of Technology.]

Copyright © 2015 Anil K Kashyap

This work is licensed under a Creative Commons Attribution 4.0 International License..

Copyright © 2015 Sapper's (Fair & Balanced) Rants & Raves

{kind=link}